At A Glance

- Most AI proofs of concept (PoCs) in banking are designed to prove capability, not production readiness. That distinction determines whether they scale

- A structured 6-week AI PoC evaluation framework closes the gap between a promising pilot and a defensible deployment

- Weeks 1–2 focus on scoping the right workflow and aligning internal stakeholders before a single line of code is written

- Weeks 3–4 shift to structured testing against real data, governance checkpoints, and explainability requirements

- Weeks 5-6 are about measuring what actually matters: not accuracy in isolation, but decision quality, audit-readiness, and adoption signals

- The output of an AI PoC should not be a demo. It should be a deployment decision.

What is an AI proof of concept in banking, and why does it keep failing?

An AI proof of concept (AI PoC) in banking is a time-boxed evaluation designed to test whether an AI solution can perform a specific task within a bank's real operational, data, and regulatory environment. It sits between an initial vendor demo and a full production deployment.

The problem is that most AI PoCs in regulated banks are not designed to answer the questions that actually determine deployment success. They are designed to look good in a review meeting.

Banks are not short of AI interest. Most have run a pilot. Many have run several. What they are short of is a repeatable way to evaluate whether a pilot is ready to become something more.

The typical pattern: a workflow is identified, a vendor is selected, a narrow dataset is prepared, and results are presented in a controlled environment. The numbers look promising. Stakeholders express cautious optimism.

Then the questions start.

How will this integrate with our case management system? What happens when the model encounters an edge case? Can we explain this output to a regulator? Who owns the decision when the AI is wrong?

These are not technical questions. They are operational and governance questions, and they are exactly where most AI programmes stall.

A well-designed AI PoC does not defer these questions to later. It surfaces them deliberately, early, and in a controlled environment where they can be answered without derailing a live deployment.

Why the standard AI PoC approach fails in regulated environments

A PoC in a consumer technology context is designed to demonstrate speed and capability. The bar is: does this work?

A PoC in a regulated bank has a higher and more complex bar: does this work, can it be explained, can it be governed, and can it be defended under audit?

The gap between these two questions is where most evaluations break down. According to McKinsey, fewer than 30% of AI pilots in financial services reach full production deployment, not because the models underperform, but because governance, integration, and adoption requirements are treated as post-pilot problems rather than PoC design inputs.

Common failure modes in regulated bank AI PoCs:

Scoping for the best case, not the real case. Curated datasets, narrow scenarios, and pre-selected cases produce results that do not reflect live conditions. When complexity returns in production, performance gaps appear quickly.

Measuring the wrong things. Accuracy rates and processing speed are useful, but they do not tell you whether an analyst will trust the output, whether a supervisor can review it efficiently, or whether a regulator can audit it.

Skipping AI governance until it becomes a blocker. Explainability, traceability, and audit trails are treated as post-pilot concerns. In regulated banking, they determine whether deployment is permitted at all, particularly under frameworks such as the EU AI Act, SR 11-7, and FCA model risk guidance.

Failing to align internal stakeholders early. Risk, compliance, IT, and operations each have legitimate concerns about AI deployment. When those concerns surface after the PoC, they become blockers rather than inputs.

The framework below is designed to address each of these failure modes, not by adding complexity, but by sequencing the right questions at the right time.

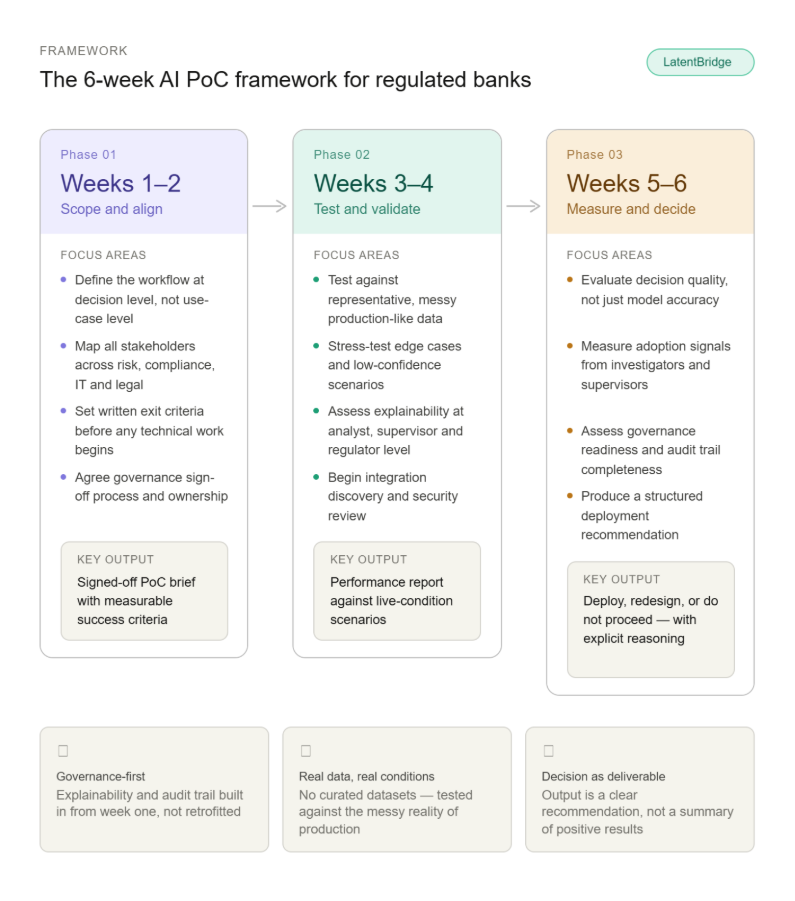

The 6-Week AI PoC Framework for Regulated Banks

The table below shows the full framework at a glance. Each phase is expanded in detail in the sections that follow.

Week 1–2: Scope and Align

Before any technical work begins, the most important work is definitional.

Define the workflow, not the use case.

AI evaluations often start with a broad use case: "improve KYC efficiency" or "reduce alert volumes." These are outcomes, not workflows. An AI PoC needs to operate at the level of a specific decision: which data inputs are used, who makes the call, what triggers escalation, and what the output needs to look like to be actionable.

Workflows in banking are layered and structured around control points. An AI that improves one step but disrupts adjacent steps creates as many problems as it solves. The scoping conversation needs to cover the full decision path, not just the target moment.

Identify the real stakeholders.

The person sponsoring the evaluation is rarely the person who will live with the outcome. In a regulated bank, a PoC that touches compliance, risk, or customer data will involve:

- The workflow owner (typically operations or a line-of-business leader)

- Risk and compliance, who will assess exposure

- IT and data, who will evaluate integration requirements

- Legal, who will assess liability and regulatory alignment

Each of these functions will have questions. The PoC is not complete until each question has a credible answer. Discovering a compliance objection six weeks into deployment is significantly more expensive than surfacing it in week one.

Set exit criteria in advance.

One of the most common AI PoC failures is ambiguous success. At the end of six weeks, stakeholders disagree on whether the results are sufficient, not because the data is unclear, but because no one agreed on what "sufficient" meant before starting.

Define exit criteria explicitly:

- What level of decision accuracy is required before production consideration?

- What explainability standard applies: model output level, case summary level, or audit trail level?

- What integration dependencies must be resolved before deployment?

- What is the governance sign-off process, and who holds it?

These are not questions for week six. They are the foundation on which the rest of the AI PoC evaluation is built.

Week 3–4: Test Against Real Complexity

This is where the technical evaluation happens, but the goal is not to demonstrate best-case performance. The goal is to stress-test the AI system against the conditions that will define production.

Use representative data, not curated data.

There is a persistent temptation in AI evaluations to prepare clean, well-labelled datasets that reflect the ideal version of the workflow. This produces results that will not survive contact with production data.

Real banking data is messy. Documents are inconsistent. Records are incomplete. Inputs arrive from multiple systems with different formats and different update frequencies. The PoC should be designed to operate under these conditions, not around them.

If data quality is identified as a significant constraint during this phase, that is important information, not a reason to pause, but a variable that needs to be factored into the deployment plan.

Test edge cases explicitly.

Every AI deployment in a regulated environment will eventually encounter scenarios the model has not been optimised for. The question is not whether edge cases exist, but how the system handles them when they do.

Design the test set to include:

- Low-confidence scenarios where the model should defer to a human reviewer

- Cases where regulatory context (jurisdiction, product type, counterparty) changes the correct response

- Scenarios involving incomplete or conflicting data inputs

How the AI system performs at its limits is often more informative than how it performs at its best.

Evaluate explainability as a first-class requirement.

Explainable AI in banking means more than a confidence score. AI outputs in compliance decisions must be defensible, not just to the team running the evaluation, but to the investigator using it daily, the supervisor reviewing cases, and the regulator reviewing the audit trail.

During weeks 3 and 4, assess explainability at each operational level:

- Can an analyst understand why a specific output was produced?

- Can a supervisor review a case and confirm the AI's reasoning was sound?

- Can the audit trail for a decision be reconstructed in a format that satisfies regulatory requirements?

Explainability that works for a technical team but not for an investigator is not sufficient. The standard is operational usability, not technical transparency.

Run integration discovery in parallel.

Technical integration is rarely a week-six conversation. Data access, API availability, security requirements, and system compatibility all have lead times that extend well beyond the PoC window.

Use weeks 3 and 4 to map integration dependencies, identify blockers, and begin the internal procurement and security review processes that will be required for production deployment. This does not need to be completed during the PoC, but it must be initiated.

Week 5–6: Measure What Actually Matters

The final phase of an AI PoC is not about generating results. It is about generating a decision.

Move beyond accuracy to decision quality.

Accuracy is a model metric. Decision quality is an operational metric. The two are related but not equivalent.

A model that achieves high accuracy on a curated test set but produces outputs that investigators cannot interpret or act on has not demonstrated operational value. The most misleading AI metrics in banking are the ones that measure the model in isolation, rather than the model within the workflow.

Evaluate decision quality by asking:

- Did AI-assisted decisions result in fewer escalations or more targeted ones?

- Did investigators spend less time validating AI outputs than they spend on manual review?

- Did the quality of case documentation improve as a result of AI-generated summaries?

- Were supervisor review cycles shorter or longer when AI outputs were present?

These questions require user involvement, not just data analysis. The PoC should include structured feedback from the investigators and supervisors who interacted with the system during weeks 3 and 4.

Assess adoption signals, not just sentiment.

Adoption is the most lagging indicator of AI success, and also the most predictive. In a six-week PoC, full adoption is not a realistic expectation. But adoption signals are.

Watch for:

- Did users actively use the system, or did they revert to existing workflows for complex cases?

- Did users modify their behaviour based on AI outputs, or did they validate everything manually?

- Did the system reduce the time investigators spent on straightforward cases, freeing capacity for more complex ones?

Low adoption during an AI PoC is not automatically a negative signal. It may indicate that integration is incomplete, training was insufficient, or the workflow design needs adjustment. Understanding the cause matters more than the adoption rate itself.

Produce a deployment decision, not a demo.

The output of an AI PoC should be a clearly structured recommendation: deploy, redesign, or do not proceed, with explicit reasoning for each conclusion.

A deployment recommendation should cover:

- Performance against the exit criteria defined in week one

- Integration requirements and estimated timelines

- Governance sign-off requirements and outstanding approvals

- Identified risks and proposed mitigations

- Recommended deployment scope: full rollout, phased, or limited pilot extension

A PoC that ends with "results were encouraging, next steps to be defined" has not completed its purpose. The decision is the deliverable.

What a good AI PoC reveals that a demo cannot

Vendor demonstrations are designed to present AI at its best: under controlled conditions, with prepared data, and with known edge cases handled in advance.

A properly designed AI PoC does the opposite. It surfaces the conditions where performance is uncertain, where integration is complex, and where governance requirements create friction.

This is not a limitation. It is the point.

Understanding what breaks first when AI is deployed in real banking environments is precisely the information needed to design a deployment that does not break. A PoC that only confirms positive results is not evaluating the system. It is extending the demo.

The banks that are moving AI from pilot to production are the ones that treat the PoC as a stress test, not a proof point.

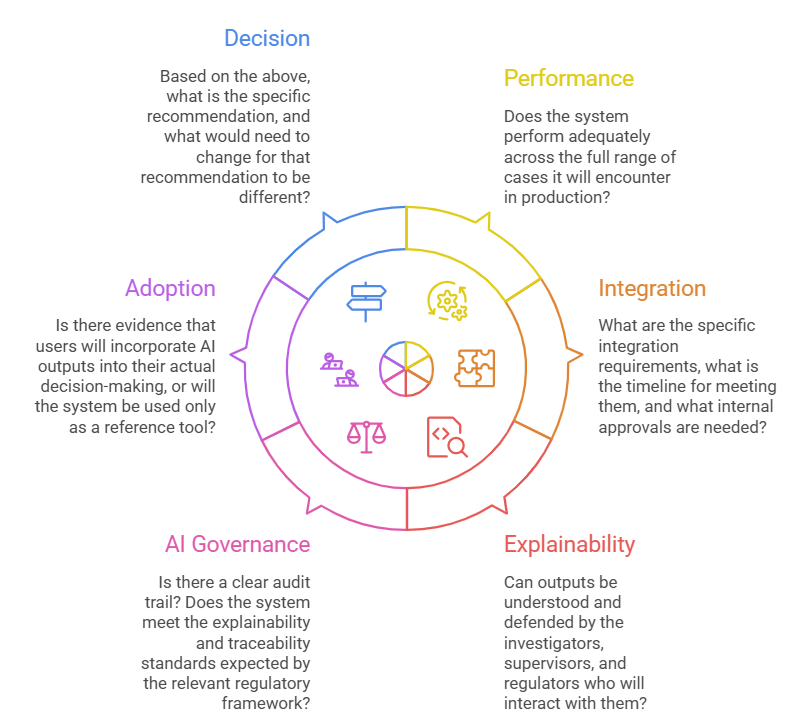

The six questions your AI PoC must be able to answer

At the end of six weeks, a well-structured AI proof of concept should provide clear answers to the following:

If an AI PoC cannot answer these questions, it has not finished.

Where AI PoCs continue to fall short

The most common failure in AI evaluation is not technical. It is structural.

Teams run PoCs to confirm decisions that have already been made, rather than to generate information needed to make them. The scope is set to favour positive results. The data is prepared to reduce complexity. The success criteria are defined loosely enough that almost any outcome qualifies.

The result is a PoC that produces momentum without producing clarity.

Selecting the right AI implementation partner is central to this. A partner whose interest is in closing a deal will design a PoC to look successful. A partner whose interest is in production outcomes will design a PoC to surface the real obstacles, because those are the obstacles that determine whether deployment succeeds.

The difference is not always visible in the demo. It becomes visible in week three.

A structured AI PoC is not a slower evaluation

There is a genuine tension in AI adoption in banking. The pace of change is fast. Competitive pressure is real. The pressure to move quickly is not irrational.

But the banks that have moved AI into production at scale are not the ones that ran the fastest PoCs. They are the ones that ran the most structured ones, designed to surface governance issues before they became blockers, integration requirements before they became delays, and adoption friction before it became inertia.

A six-week AI PoC framework does not slow down adoption. It removes the friction that causes programmes to stall at six months.

The shift from AI as a cost centre to a strategic partner does not happen through faster pilots. It happens through deployments that hold up under operational conditions, regulatory scrutiny, and the day-to-day realities of how banking teams actually work.

That starts with knowing what you are evaluating, and how.

How LatentBridge approaches AI PoCs in regulated banks

Most AI vendors run a PoC to win a deal. LatentBridge runs a PoC to answer a question: is this ready for production, and if not, what needs to change?

As a full-stack AI innovation partner working with banks, financial institutions, and law firms, LatentBridge designs every evaluation around the operational, governance, and integration requirements that determine whether AI holds up in a regulated environment, not just whether it performs well in a controlled test.

That means scoping against real workflows, not curated scenarios. Testing against representative data, not ideal datasets. And producing a deployment recommendation, not a demo.

Our AI Labs methodology is built around the workflows where the stakes are highest: sanctions alert triage, KYC and client onboarding, and finance operations. Each has been designed to surface the friction that most PoCs defer, so that the path to production is clear before a single line of production code is written.

If you are planning an AI proof of concept and want a framework built for production readiness from week one, speak with our team or start with an AI Assessment to identify where the highest-value, lowest-risk entry point is for your organisation.