At A Glance

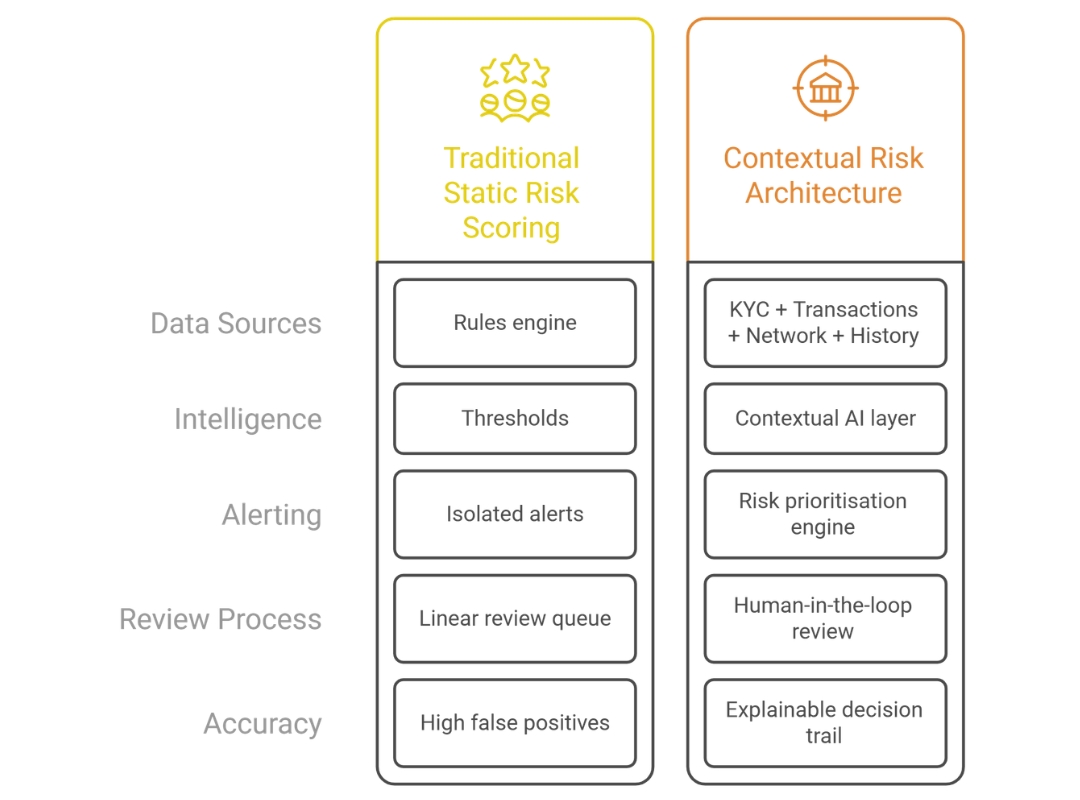

Static risk scoring frameworks built on fixed thresholds and additive models were designed for slower, more predictable financial environments. In today’s landscape, financial crime risk is increasingly relational, behavioral, and time-dependent, making static scoring insufficient for effective prioritisation.

Contextual Risk Architecture introduces a governed layer that interprets risk signals across KYC data, transaction behavior, network exposure, and historical case outcomes. Rather than replacing existing monitoring or screening systems, it strengthens how alerts are sequenced, explained, and reviewed under regulatory scrutiny.

For banking and financial services leaders, the shift is not about adopting AI for scoring alone, but about improving the structure, defensibility, and consistency of risk interpretation across financial crime workflows.

For years, financial crime programs in banking have relied on static risk scoring frameworks built around thresholds, weightings, and additive models. These models classify customers and transactions into predefined risk categories unless manually reviewed, creating a sense of control and auditability that has historically satisfied regulatory expectations.

This approach worked well in slower, more predictable environments where financial crime signals evolved gradually and operational complexity was manageable. However, the landscape has changed. Risk today is more interconnected, behavioral, and cross-border than ever before.

The core issue is no longer whether banks have scoring models. Most do. The real question is whether those models reflect how risk actually behaves in modern financial ecosystems.

Risk does not emerge as isolated indicators. It develops through relationships, behavioral shifts, network exposure, and contextual signals over time. Static scoring frameworks, by design, struggle to capture this dynamic reality.

The Structural Tension Inside Financial Crime Programs

Compliance leaders across banking institutions are navigating a persistent operational tension. When thresholds are tightened, alert volumes surge and investigative teams are burdened with low-quality reviews. When thresholds are relaxed, internal stakeholders grow concerned about missed exposure and regulatory defensibility.

This dilemma is often framed as a calibration problem. In reality, it is an architectural one.

Static scoring models interpret risk as a snapshot taken at a single point in time. Modern financial crime, however, behaves more like a narrative that unfolds across transactions, entities, and jurisdictions. When institutions rely solely on static indicators, they often struggle to prioritise alerts in a way that reflects true risk significance.

The result is not just operational fatigue. It is inconsistent sequencing of risk, where high-risk cases do not always surface first.

From Risk Snapshots to Contextual Risk Narratives

Traditional scoring models are designed to answer a narrow question: does a transaction or customer trigger predefined indicators? Contextual risk scoring expands this perspective by evaluating signals in combination and over time.

Instead of assessing isolated triggers, contextual models consider behavioural baselines, peer comparisons, network relationships, jurisdictional exposure, and historical investigative outcomes. This enables institutions to interpret activity patterns rather than single events.

This shift is subtle in theory but profound in practice. Risk is no longer treated as additive and static. It becomes relational, evolving, and context aware.

For compliance teams, this does not mean abandoning rules. It means strengthening how those rules are interpreted within a broader risk narrative.

Why Supervisory Expectations Are Quietly Evolving

Regulators rarely prescribe specific technologies, but they consistently emphasise outcomes such as risk-based prioritisation, proportionality, ongoing monitoring, and defensible reasoning. These expectations implicitly favour approaches that can adapt to changing risk patterns rather than rely solely on fixed thresholds.

Global supervisory discourse aligned with Financial Action Task Force risk-based principles and analytical perspectives from institutions such as the Bank for International Settlements increasingly highlights the importance of dynamic monitoring and contextual interpretation of risk.

The direction is becoming clearer. Institutions are expected to demonstrate that their risk frameworks evolve alongside emerging typologies and behavioural complexity.

Static models may remain compliant, but static prioritisation is becoming harder to justify.

The Hidden Limitation of Threshold-Centric Risk Models

Many institutions believe that continuous threshold tuning reflects model maturity. In practice, this often creates structural blind spots rather than genuine intelligence.

Static scoring frameworks struggle to detect behavioural drift over time, overlook indirect network exposure, and generate large volumes of alerts that dilute analyst attention. When alert queues grow, investigative quality becomes uneven, and truly high-risk cases may not receive timely prioritisation.

This creates a paradox. On paper, the control framework appears robust. Operationally, risk interpretation becomes reactive and resource-intensive.

Contextual risk architecture addresses this limitation by improving how risk is sequenced and interpreted, not merely how it is detected.

Governance as the Deciding Factor in Contextual AI Adoption

The introduction of contextual AI into financial crime workflows inevitably raises governance concerns, particularly around explainability and auditability. In regulated banking environments, contextual scoring cannot operate as a black box.

It must provide transparent signal attribution, clear reasoning trails, policy traceability, and documented override mechanisms. Human-in-the-loop validation remains essential, especially for high-risk decisions and regulatory reporting.

Effective contextual risk architecture is therefore not just a modelling exercise. It is a governed framework that is explainable by design, tunable without reengineering, version controlled, and auditable at the decision level.

When governance is embedded within the workflow rather than layered on top, contextual intelligence strengthens control instead of introducing ambiguity.

Operational Realities Institutions Encounter During Implementation

Contrary to common assumptions, the primary barrier to contextual risk scoring is rarely model sophistication. More often, it is data coherence.

Contextual interpretation depends on reliable KYC baselines, clean entity resolution, consolidated customer profiles, structured case histories, and clear data lineage across systems. Where data remains fragmented, contextual models expose inconsistencies that static scoring frameworks previously masked.

While this exposure can initially appear challenging, it often provides valuable diagnostic clarity. Institutions gain visibility into structural data gaps that directly impact risk interpretation and investigative efficiency.

The Commercial and Operational Impact of Contextual Risk Architecture

When implemented within a governed framework, contextual risk architecture delivers measurable operational improvements. Institutions typically observe reduced false positive volumes, improved alert prioritisation accuracy, and shorter investigation cycles.

Analyst rework declines as contextual insights reduce repetitive reviews and improve decision consistency. Onboarding and monitoring workflows become more proportionate, allowing low-risk cases to be resolved faster while genuinely high-risk exposures receive earlier attention.

The most significant impact, however, is not speed alone. It is confidence under scrutiny. Compliance teams gain stronger assurance that prioritisation decisions are consistent, explainable, and defensible during audits and regulatory reviews.

Where Contextual Risk Architecture Becomes Operational

Contextual risk scoring should not be viewed as a standalone model upgrade. It represents a structural decisioning layer that sits between detection systems and human disposition.

In practice, this layer connects KYC data, sanctions exposure, transaction behaviour, network relationships, and historical case outcomes into a governed prioritisation framework. Existing monitoring and screening systems remain in place, but their outputs are interpreted with greater context and consistency.

Institutions often begin by applying contextual logic within a single workflow such as onboarding, transaction monitoring, or sanctions review. Over time, the value compounds as contextual interpretation becomes consistent across multiple financial crime streams.

This is less about orchestration as a technical ambition and more about coherence in how risk is interpreted across teams, systems, and jurisdictions.

The Strategic Question for Compliance Leaders in 2026

Static scoring frameworks will continue to play a foundational role in financial crime programs. However, relying on them in isolation is becoming increasingly insufficient in an environment where risk evolves faster than rule updates and regulatory scrutiny demands more nuanced interpretation.

The critical question is no longer whether AI can score risk. It is whether static scoring alone adequately reflects the complexity of modern financial crime exposure.

Contextual risk architecture does not replace human judgment. It strengthens it by providing structure, consistency, and defensible reasoning.

In a regulatory climate where accountability is personal and scrutiny is continuous, structured and contextual interpretation of risk is rapidly shifting from innovation to operational necessity.

Editor’s Note

This perspective reflects work across regulated financial environments designing structured frameworks for contextual risk interpretation, governance integration, and cross-workflow prioritisation. The approach emphasises explainability, domain logic, and human-in-the-loop safeguards aligned with supervisory expectations in banking and financial services.